myBSN: Cara Daftar BSN Online Banking & Login Akaun

Kini kita dah tak perlu ke kaunter lagi untuk daftar BSN online melalui portal myBSN.

Seperti mana bank-bank lain di Malaysia, Bank Simpanan Nasional atau BSN juga menyediakan khidmat perbankan online yang mudah dan cepat.

Selain digunakan untuk menjalankan transaksi kemasukan, pengeluaran dan pemindahan wang, BSN online juga biasa digunakan untuk tujuan pembelian pin Unik UPU.

Berikut adalah maklumat lanjut tentang myBSN serta langkah pendaftaran yang lengkap dan mudah.

Apakah myBSN?

Ianya merupakan portal internet yang mengandungi semua perkara tentang BSN termasuklah maklumat korporat serta produk dan perkhidmatan yang ditawarkan.

Kita juga boleh menjimatkan masa dengan pelbagai pautan perkhidmatan perbankan BSN online melalui internet seperti:

- Pertanyaan Baki

- Pemindahan Dana

- Pembayaran Bil

- Pembayaran Kad Kredit

- Pembelian SSP

- Pembelian Pin

- dan banyak lagi.

Cara Daftar BSN Online @ myBSN

Sebelum mula daftar BSN online, pastikan kita dah ada kad ATM dan ingat nombor telefon yang didaftarkan.

Jika tidak, sila ke kaunter BSN untuk daftar / tukar nombor telefon bagi membolehkan proses daftar BSN online.

Trending sekarang

LANGKAH 1

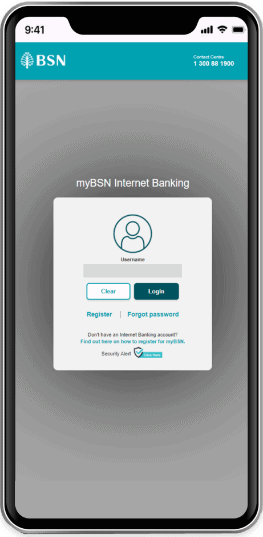

Untuk daftar BSN online sila layari laman web mysBSN di:

Klik ‘Register’.

Tandakan butang ‘Accept’ untuk ‘First Time Registration’.

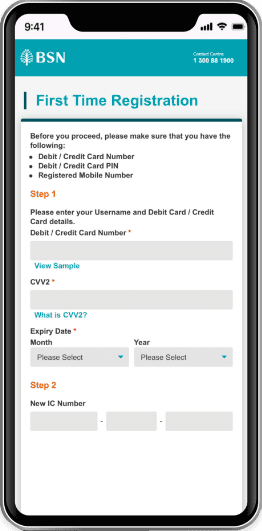

LANGKAH 2

Masukkan maklumat: Nombor Kad Debit / Kad Kredit, Nombor Pin (untuk Kad Debit Sahaja), tarikh tamat tempoh Kad dan CVV2.

Masukkan 16 digit no kad bank anda yang tertera pada kad ATM.

Kemudian isikan nombor cvv2 (3 nombor di bahagian belakang kad ATM anda) serta tarikh sah tempoh kad anda (valid thru).

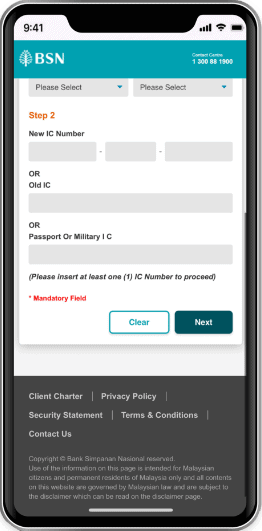

LANGKAH 3

Masukkan nombor Kad Pengenalan baru / Kad Pengenalan lama / nombor Passport.

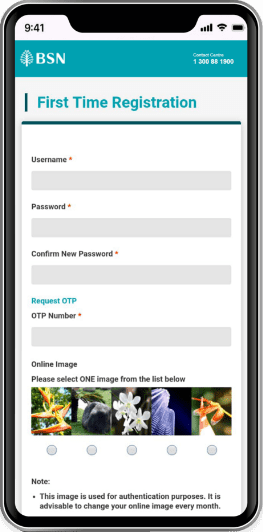

LANGKAH 4

Masukkan username / ID pengguna yang dipilih beserta kata laluan.

Tekan ‘Request OTP’.

Nombor OTP akan dihantar ke telefon bimbit melalui SMS.

Masukkan 6 nombor tersebut untuk meneruskan pendaftaran.

Kemudian pilih 1 ‘online image’ yang mudah diingat (bagi tujuan pengesahan nanti).

SELESAI

Jika pendaftaran berjaya, skrin anda akan memaparkan pengesahan pendaftaran beserta butiran maklumat had transaksi perbankan.

Anda boleh login semula dan melihat senarai akaun di menu ‘Account Overview’.

Sila rujuk panduan video di bawah :

Cara Login MyBSN Pertama Kali

Anda perlu login semula dengan menggunakan username dan password tadi.

Sebagai pengguna pertama kali, anda perlu mengisi data peribadi yang diminta di kotak bertanda *.

Butiran lain boleh juga diisi jika mahu.

Selepas itu, anda sudah boleh memulakan transaksi online BSN internet banking!

Trending sekarang

Jika anda terlupa KATA LALUAN atau ID yang didaftarkan, sila rujuk : Lupa Kata Laluan BSN Online? Ini Cara Tukar Password MyBSN

Perkhidmatan Perbankan Internet BSN

Setelah login, anda boleh mengakses dan pelbagai maklumat akaun BSN anda dan melakukan aktiviti perbankan seperti:

i) Pemindahan Dana

Had maksimum harian untuk Pemindahan Dana bagi pihak ketiga ialah RM10,000.

Tiada apa-apa caj dikenakan bagi pemindahan antara akaun BSN.

ii) Semak Rekod Transaksi

Selepas anda log masuk, pergi ke Account Overview dan klik akaun pilihan.

Kemudian, klik ‘View MyBSN Transaction History’. Anda akan dapat lihat pembayaran yang dibuat sejak 60 hari lepas.

iii) Pembayaran Pinjaman

Dengan IBG, anda boleh melaksanakan pemindahan dana serta pembayaran kad kredit, pinjaman dan bayaran ansuran sewa beli kepada bank lain yang tersenarai.

Had maksimum harian untuk Transaksi IBG ialah RM10,000.00.

Baca juga : Cara Semakan Baki PTPTN Online & Tunggakan Terkini

iv) Pembayaran Bil

Kemudahan pembayaran yang membolehkan anda membayar bil kepada badan-badan penerima yang tersenarai melalui myBSN.

Perkhidmatan Pembayaran Bil kami adalah percuma.

v) Pembelian Pin

Dengan BSN, anda boleh membeli PIN UPU online untuk diri sendiri atau orang lain.

Cuma masukkan nombor Kad Pengenalan pelajar/calon.

SSP BSN direka khusus untuk pelanggan BSN sahaja.

Anda mesti ada Kad ATM BSN yang sah dan mendaftar sebagai pengguna Perbankan Internet sebelum membeli SSP secara online.

Semak dan sahkan alamat anda terlebih dahulu sebelum meneruskan pembelian SSP.

Tiada had untuk pembelian SSP melalui myBSN.

Baca juga : Cara Buat Link Whatsapp (Tak Perlu Save Nombor)

Maklumat Lanjut

Jika ada masalah untuk log masuk, sila hubungi Pusat Khidmat Pelanggan myBSN di talian 1300 88 1900 atau +603-2613 1900 (Luar negara).

Trending sekarang

Talian ini dibuka 24 jam sehari.

Untuk melihat Soalan Lazim tentang cara daftar BSN online dan perkhidmatan yang disediakan, sila rujuk di pautan berikut: https://www.bsn.com.my/page/faq?lang=ms-MY&csrt=1467993480280683042

Untuk maklumat lanjut berkaitan perkhidmatan daftar BSN online, layari info penuh di https://www.mybsn.com.my/